KiwiSaver funds continue to ride the wave of buoyant stock markets with all funds making positive returns to the quarter ending June 30.

According to the latest Morningstar quarterly KiwiSaver Survey released this week, all multisector KiwiSaver funds made positive returns with average category returns ranging from 1.6% for the conservative category and up to 5.8% for the aggressive category.

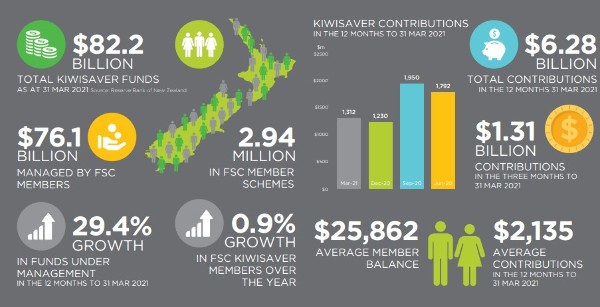

Morningstar's Asia-Pacific director of manager research Tim Murphy says total KiwiSaver assets continue to grow and are close to reaching $83 billion.

Murphy says Morningstar agrees with the Financial Markets Authority's recent guidance to KiwiSaver providers on the inappropriateness of marketing shorter-term periods, like 12-month returns, as a means of attracting new prospective investors.

"And as we have repeatedly reiterated every time we publish our quarterly KiwiSaver Survey, 'it is most appropriate to evaluate performance of a KiwiSaver scheme by studying its long-term returns'."

Murphy says worldwide equity markets generally made positive returns over the June quarter, as economies continue to open and recover, vaccine rollouts expand and more people return to the workplace, against this backdrop the MSCI World Index was up 8.0% in NZD.

The US market ended the quarter up 8.6% and almost all sectors made positive gains, led by real estate and technology sectors.

"KiwiSaver funds generally reflected the underlying market conditions experienced over the June quarter with all multisector funds posting positive returns," says Murphy.

"Funds with larger exposures to international growth assets generally outperformed over the three-month period.

"Top performers over the quarter against their peer group includes ANZ Default Conservative 2.3% (Multisector Conservative), OneAnswer Conservative Balanced 3.0% (Multisector Moderate), ASB Positive Impact 4.9% (Multisector Balanced), AMP ANZ Growth 5.9% (Multisector Growth), and Milford Aggressive 7.8% (Multisector Aggressive)."

Over 10 years, the growth category average has given investors an annualised return of 10.5%, followed by Aggressive (10.3%), Balanced (8.7%), Moderate (6.6%), and Conservative (5.9%)

KiwiSaver assets on the Morningstar database sit at more than $82.9 billion as of June 30, up from $76.3 billion on December 31, 2020.

ANZ leads the market share with more than $18.5 billion. ASB is in second position, with a market share of 17.1%.

Westpac holds third spot ahead of Fisher Funds, while AMP sits in fifth.

The six largest KiwiSaver providers account for approximately 74% of assets on the Morningstar database.