Bumping up KiwiSaver contributions and introducing a carer’s savings credit for those with young children are among the improvement measures identified in a new report benchmarking New Zealand against other countries’ pension systems.

The Mercer CFA Institute Global Pension Index compares 48 retirement income systems based on their adequacy, sustainability and integrity. New Zealand is ranked 14 out of 48 overall, landing in the top 20 for both sustainability and integrity, but slipped from 25th last year to 28th in 2024 for adequacy. New Zealand’s placing earns it a “B” grade.

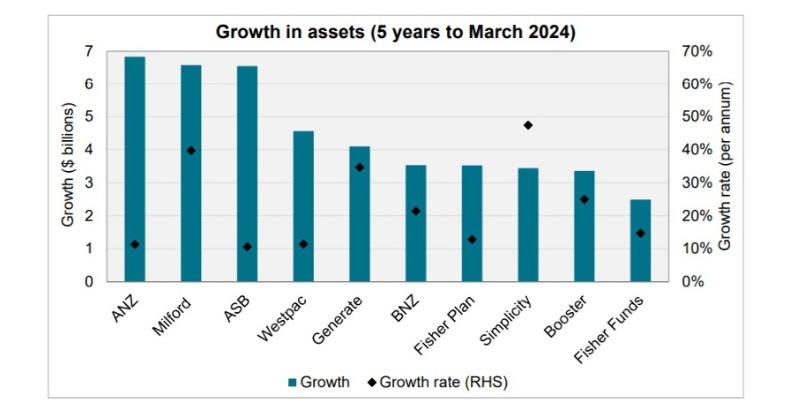

“KiwiSaver is the fastest growing invested asset in the country, having surpassed $100 billion NZD,” said Mercer New Zealand’s Consumer Wealth Leader Sarah Whitelock.

“As the KiwiSaver system matures, and we are starting to see the benefits play out for retirees through a supplemented retirement income, we now need to ensure that savers of all ages understand the importance of retirement planning and decumulation strategies.”

A focus on ensuring people understand retirement income is the core purpose of KiwiSaver would help improve the system, as well as further education for savers on how to turn their nest egg into an income during retirement.

Other improvements to the system are outlined in the report and include increasing the level, coverage and tax efficiency of KiwiSaver contributions, encouraging households to save more money and reduce debt levels and introducing a savings credit or contribution for carers of young children, which is not contingent on them making their own contribution.

Topping the global pension rankings was the Netherlands, followed by Iceland, then Denmark.

Rise of defined contribution plans adds complexity

At a global level, the report acknowledges retirement systems are increasingly moving away from defined benefit plans in favour of defined contribution plans, like KiwiSaver.

CFA and CFA Institute’s President and CEO Margarent Franklin said the shift creates challenges to financial planning, and future retirees will be the ones forced to deal with them.

“DC plans require individuals to make complex financial planning decisions that may significantly impact their financial circumstances, and yet many individuals are not well prepared to manage the required decisions.”

“The Index serves as an important reminder of the gaps that remain in providing long-term financial security and advice for individuals. The need for credentialed and ethical financial advisors once again stands out, and that’s why we have launched new initiatives in the private wealth space to meet this gap,” she said.