Over the lifecycle of a KiwiSaver investment switches will be required at key investor milestones but these can be clunky. Michael Lang talks about the alternatives

By now many New Zealanders have successfully navigated their way out of the default scheme they were randomly allocated to, into more growth-orientated schemes. The move has been a good one, with investors accumulating at least an additional $800 million over the past three years, based on NZ Funds’ estimates. But will it be a case of out of the frying pan and into the fire?

Growth-orientated schemes can be a double-edged sword; while their returns are higher than income-orientated schemes over the long-run, they can deliver significant losses over the short term. In some cases shares, the primary driver of growth schemes, can take more than a decade to recover from a slump. And the recovery times assume investors do not panic and switch to cash, and do not make any withdrawals from their scheme until it has fully recovered.

This is bad news for New Zealanders approaching retirement. To get the most out of their scheme, most New Zealanders will need to make at least two KiwiSaver switch decisions in their lifetime, more if they use KiwiSaver for their first home purchase.

The first switch is likely to be out of a default scheme into a growth scheme. This increases the value of their account at retirement. A second switch decision should then be made thirty or forty years later as they approach retirement. This is a switch out of a growth into a more balanced scheme (that is a mix of income and growth assets). This switch helps preserve the capital sum they have accumulated and prepares the assets for the regular withdrawals that will fund their retirement.

So far, most KiwiSaver decisions have been DIY. The FMA’s 2015 review of KiwiSaver providers found that only three out of 1000 New Zealanders receive advice when joining KiwiSaver or transferring between schemes. Today, this should be higher given some of the changes the FMA have made, but anecdotally the vast majority of New Zealanders do not receive advice.

Unfortunately, as KiwiSaver balances grow, so do the consequences of making a poor financial decision. And investors need only make one poor investment decision, for example a switch from growth to income in the middle of a share market slump, to ruin a lifetime of investing. This is why target-date or lifecycle funds have taken off in America since the share market collapse in 2009. Since then, the total assets in lifecycle funds have grown from $158 billion to over $1.10 trillion at year-end 2018 according to ICI and Morningstar Inc.

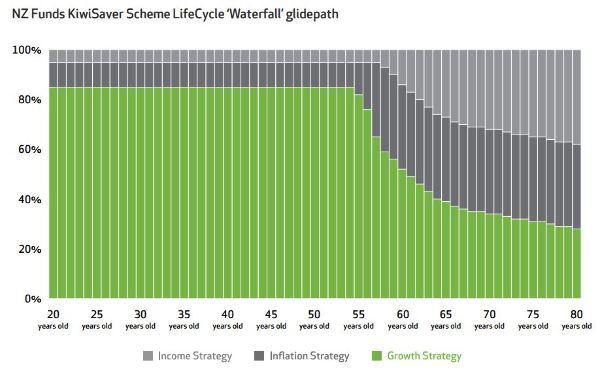

Out of the 30 schemes offered to New Zealanders to meet their retirement objectives, only nine have lifecycle options1. Of these, only one scheme (NZ Funds KiwiSaver Scheme) offers a waterfall asset allocation that ensures clients are rebalanced every twelve months for a lifetime. All other lifecycle schemes in New Zealand use periodic step changes to asset allocation, made popular in the late 1990’s by Donald Luskin and Larry Tint of Wells Fargo Investment Advisors. Overseas, such schemes have waned in popularity due to the fact that significant market movements can leave these clunkier schemes over or underweight an asset class for years at a time. NZ Funds KiwiSaver Scheme’s LifeCycle ‘Waterfall’ glidepath overcomes this obstacle.